GLOBAL steel giant ArcelorMittal announced on Thurday(11) that Aditya Mittal, the son of company founder Lakshmi Mittal, will replace him as the group's chairman and CEO.

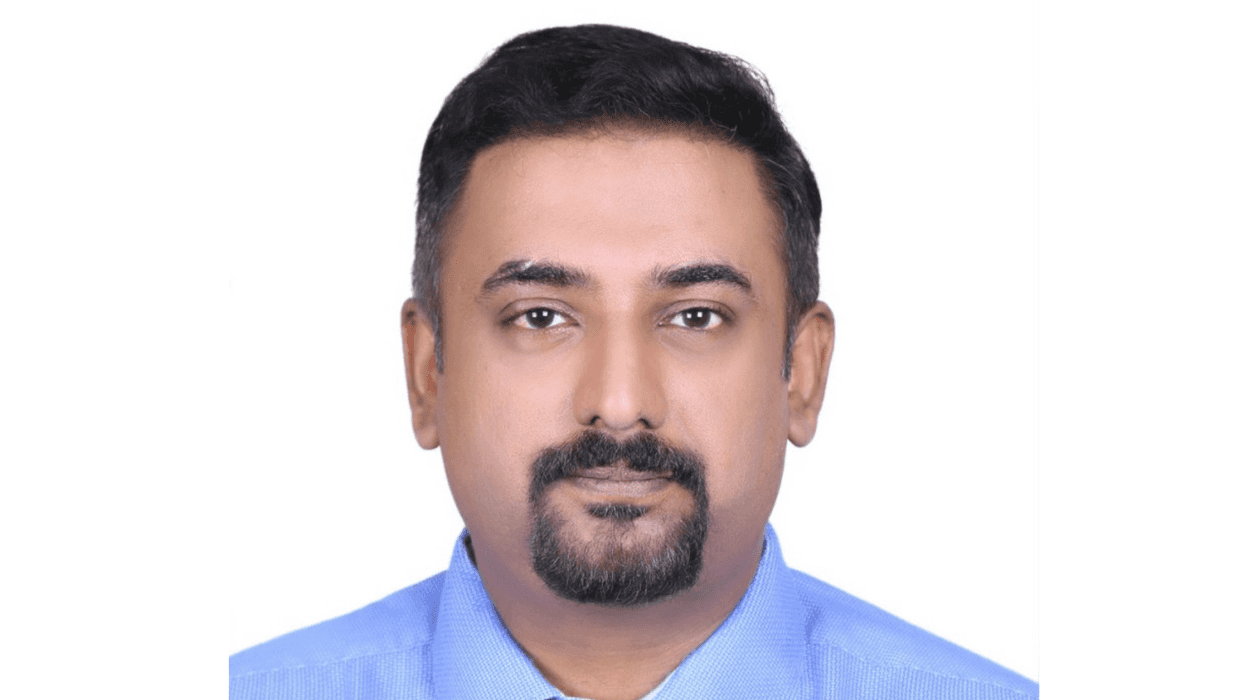

Currently, he is the chief financial officer (CFO) of the firm and will be replaced by Genuino Christino.

The elder Mittal, who founded the company in 1976, will become executive chairman of the Luxembourg-based company.

He will continue to lead the board of directors and work together with the CEO and management team, a statement said.

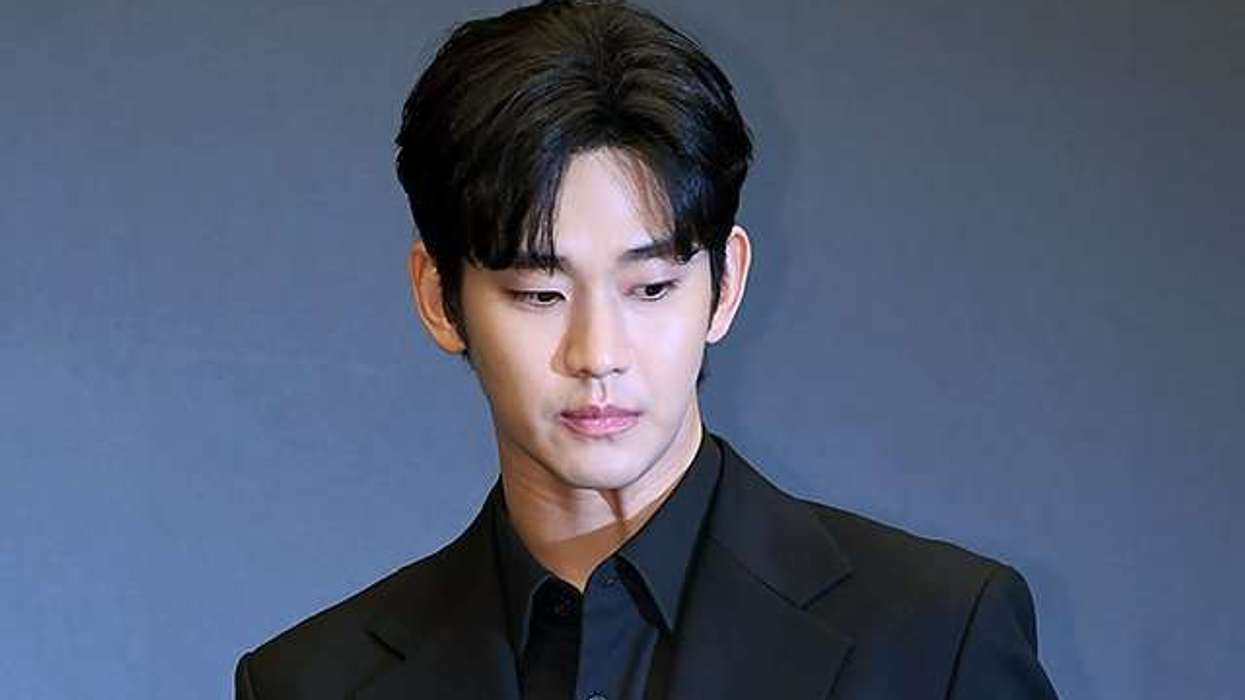

"It is an honour to be the CEO of the world's largest steel making company. Mr Mittal built ArcelorMittal from a greenfield rolling mill in Indonesia. It is an extraordinary achievement and I am privileged to have witnessed and been part of so much of that journey," said Aditya Mittal.

"The world is transforming at a rapid pace and it brings challenges but also many opportunities for ArcelorMittal. The biggest challenge, but also the biggest opportunity, will be to demonstrate that steel can de-carbonise and indeed is the perfect material for a circular economy."

Aditya Mittal joined his father's firm from Credit Suisse and was involved in the 2006 merger of Arcelor and Mittal Steel, which created the current company.

The announcement came as the company said it had reduced it's net loss in 2020 by a factor of three to $733 million, even though sales dropped by a quarter.

Despite the worldwide coronavirus slump, ArcelorMittal returned to profit in the fourth quarter of last year.

Looking forward to 2021, the company expects global steel demand to increase by between 4.5 and 5.5 per cent, after it dropped by one percent in 2020.

Lakshmi Mittal said he was proud of the group's performance and that he was pleased to be handing on the reins "in a position of relative strength."

"The board unanimously agree that Aditya Mittal is the natural and right choice to be the company's chief executive," the chairman said.

"We have worked closely together since he joined the company in 1997, indeed in recent years we have effectively been managing the company together."