OYO Hotels and Homes becomes the latest firm in India to announce a pay cut due to the ongoing COVID-19 crisis.

The softbank-backed company has cut the salaries of all employees by 25 per cent for four months starting April.

Besides, it sent some of its workers on leave with limited benefits, reports Reuters.

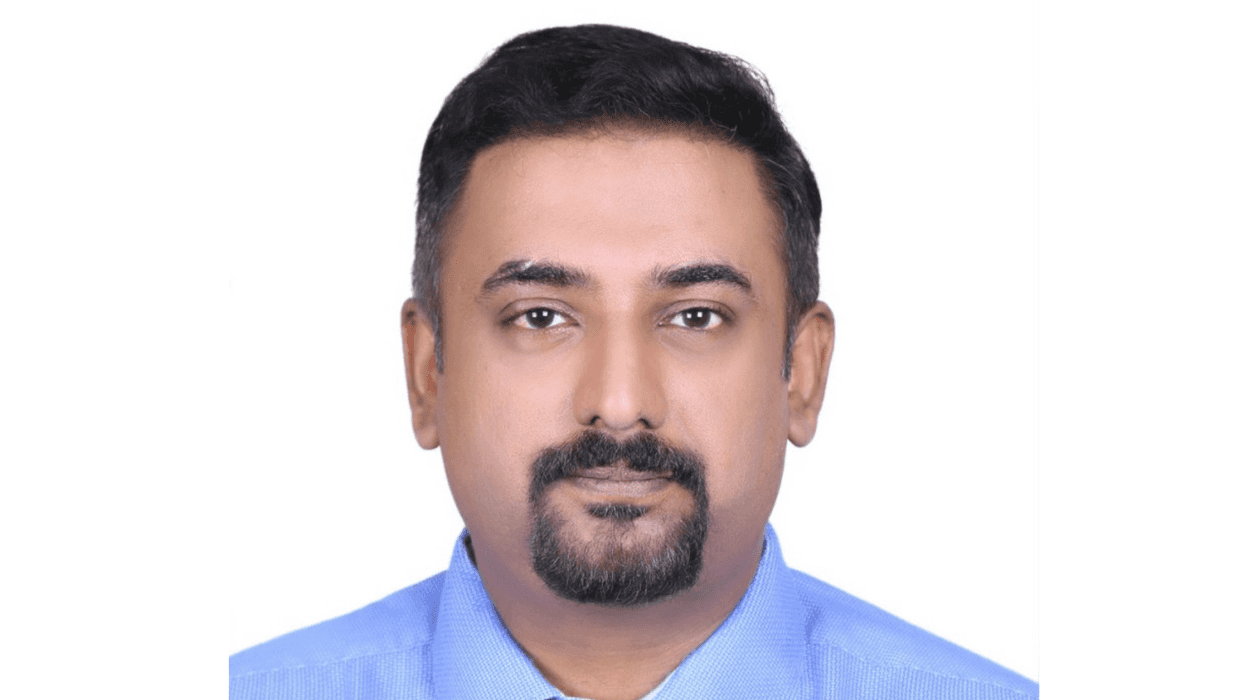

Rohit Kapoor, chief executive of OYO, said, "Our company is taking a difficult but necessary step for India, whereby we are asking all OYOprenuers to accept a reduction in their fixed compensation by 25 per cent".

Some employees will also be placed on leave with limited benefits from May 4 and until August, Kapoor said.

Earlier in April, OYO furloughed thousands of its international employees after the COVID-19 outbreak brought global travel to a halt.

Globally, the hospitality sector is witnessing a severe crisis due to the pandemic.